The Long-term Dangers of Trump’s Big Beautiful Bill

Analysis shows that the bill would weaken US economic, fiscal and institutional resilience

The House just passed the One Big Beautiful Bill by the slimmest of margins. At a high level, the Bill extends and expands expiring tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA), and partially pays for it with large cuts to Medicaid and the Supplemental Nutrition Assistance Program (SNAP), among other social programs. Contrary to claims of deficit reduction by the Bill’s supporters, the nonpartisan Congressional Budget Office (CBO) forecast that the Bill would add $3.8 trillion to the debt over 10 years, and increase economic inequality.

Such a large regressive transfer would come at the cost of long-term national economic, fiscal, and democratic institutional resilience.

A macro-fiscal lens

To see why the Bill is especially harmful for long-term economic and fiscal resilience, it’s helpful to decompose the evolution of national debt as a fraction of GDP (i.e., the debt ratio) into three basic parts: nominal GDP growth (g), the cost of debt (i.e., the interest rate, r), and annual deficits as a share of GDP (d). Roughly speaking, the debt ratio will stabilize if (r-g) + d is less than 0, and will rise if it's greater than 0.

Currently, (r-g) is forecasted to average about -0.6% over the next 10 years, meaning that without deficits, the economy would outgrow the accumulation of debt, by a slim margin. However, even before the Bill, deficits are forecasted to add about 2% of GDP annually to national debt, pushing us over this sustainability threshold, leading to an escalating debt ratio.

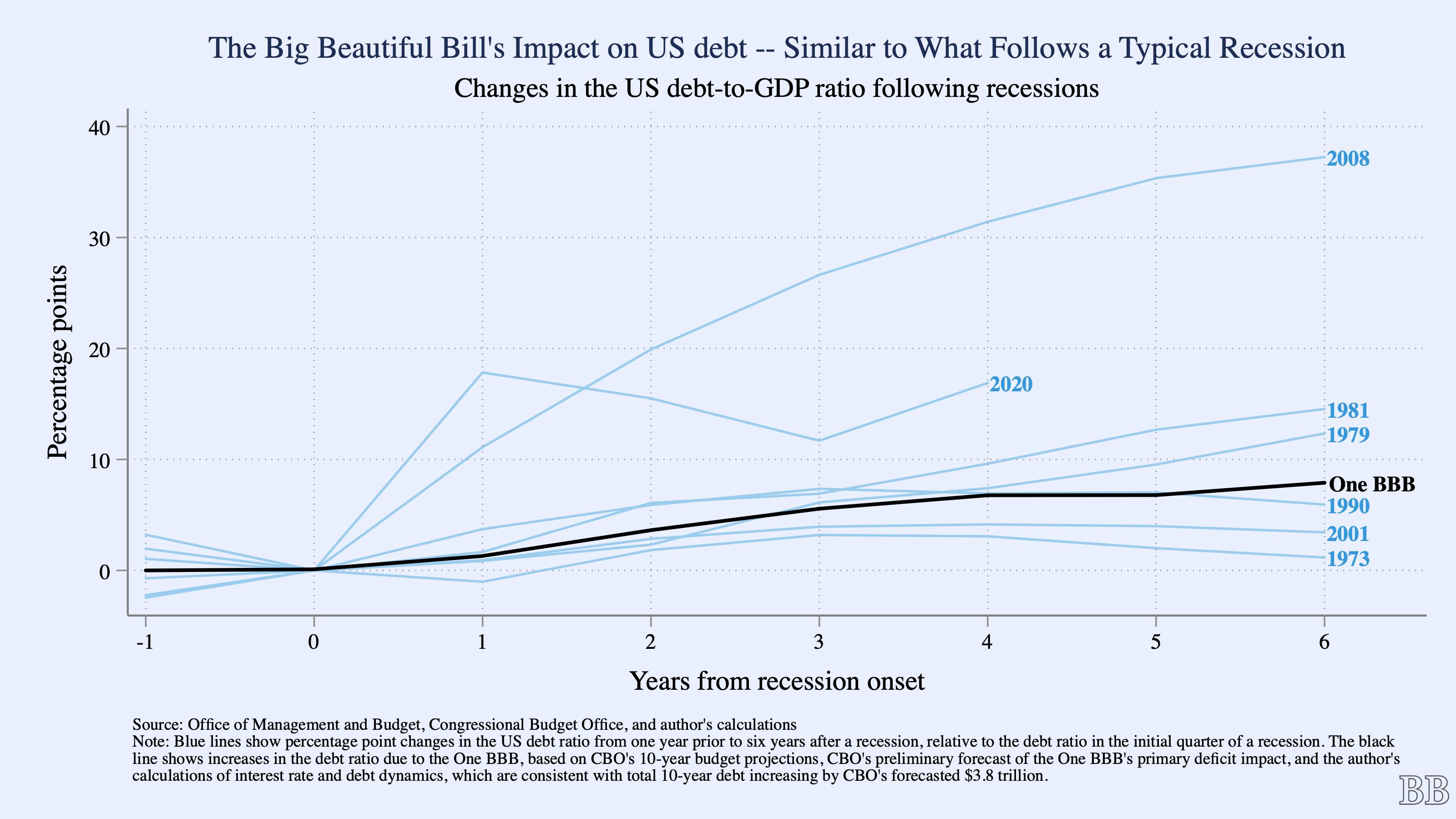

The US debt ratio is forecasted to be about 100% this year, grow to 118% by 2035, and continue to escalate throughout CBO's 30-year outlook. Like the boiling frog, escalating debt matters because it will increasingly harm everyday borrowing costs, suppress economic opportunities, and limit the government’s ability to make essential investments and respond to future crises.

Sound fiscal policy would make critical investments to grow the economy (g), strengthen economic resilience (which insulates g from economic shocks and lowers r), and reduce deficits (d). As I’ll explain below, along each dimension, the House Bill does precisely the opposite.

Growth and deficit effects

Simple rule-of-thumb math can dispel the notion that the Bill’s $4.5 trillion in tax cuts can remotely pay for themselves. With GDP at $30 trillion dollars, and with tax revenues at about 17% of GDP under the Bill, GDP levels would have to be 6% higher in each year to generate enough additional tax revenue to cover the stream of roughly average annual $350 billion in primary deficits.

To put this in context, the Penn Wharton Budget Model forecasts that GDP would be only 0.5% higher by 2034 as a result of the Bill. The Congressional Budget Office (CBO) forecast similarly small GDP effects. Claims that the Bill’s tax cuts will pay for themselves are based on wildly unrealistic GDP growth assumptions and misleading accounting gimmicks.

Moreover, primary deficits (d) resulting from the Bill would add about 1% of GDP higher each year. This increase, alone, swamps the current slim (r-g) margin, even before factoring in higher interest rates and compounding debt dynamics. Factoring those in, CBO forecasts the Bill would add $3.8 trillion to the debt over 10 years. The increase in the debt ratio would be similar to what follows the typical US recession, and higher than what follows every recession over the past half century other than the Great Recession and those associated with historic supply shocks (see figure, below).

Why are growth impacts of the Bill so tiny? Investment crowdout and worrisome interest rate impacts

Lower taxes can drive investments, and therefore growth, but any growth effect of the Bill would largely be offset by headwinds from increased debt. In principle, capital needed to pay now-higher debt would crowd out some investments, and simultaneously raise interest rates, adding to the cost of debt. It's also unclear what productivity would be for any new investments by firms that currently enjoy the highest liquidity in three generations, and pay historically low levels of taxes despite high profitability.1

Economists have estimated how debt will reduce investments, with consequent increases in interest rates, with larger reductions in investments in response to deficit-financed tax cuts, as in this Bill.2 But in truth, there is no empirical precedent for how trust in the world’s largest economy, and its ability to manage short-run fiscal imbalances, might unwind. While trust has historically been rock solid, amid increases in the US debt ratio and inaction to reverse fiscal imbalances, it's starting to wane.

To get a sense for how profligate and concerning the Bill is, its $4.5 trillion in tax cuts is ten times greater than the cost of the “once-in-a-generation” investment in public infrastructure from the Bipartisan Infrastructure Law—a law that CBO forecasted as having sizable long-term growth benefits outside the 10-year budget window.

The shocking disregard for prudent fiscal policy in the House bill, and the political dynamics that propel it, are raising red flags in financial markets, potentially signaling a turning point in rate responsiveness to US fiscal imbalances. Indeed, the Bill’s progress through Congress has rattled bond markets and raised interest rates, with concerns over its passage contributing to muted demand in last Wednesday’s Treasury auction. Recent rating downgrades of US debt, by Fitch, S&P, and last week by Moody's, highlight these growing concerns.

The Bill harms economic resilience

With no effects on growth, and harmful effects on deficits and interest rates, does the Bill achieve anything? The CBO, Penn-Wharton, and the Joint Committee on Taxation (JCT) forecast that the Bill would primarily achieve unprecedented transfers to the wealthiest individuals and the most profitable corporations, paid for in part by lower-income individuals.

As a result of the Bill, most Americans will experience a continuation of tax cuts from the TCJA, making the $4.5 trillion cost of extending and expanding TCJA tax policies an easier sell. But the vast majority of the tax cuts would accrue to the highest income earners. Relative to current law, the typical tax filer will get about $800 in 2027, while those in the top 0.1% will get $390,000. According to the JCT, the 194,000 filers in the top 0.1% would collectively see their taxes cut by about $50 billion in 2027, equal to the tax cuts that would accrue to the bottom half of all taxpayers—or about 95 million filers.

On top of this, the Bill cuts $1.2 trillion in Medicaid and SNAP spending. Accounting for these cuts, the Bill would reduce net resources to the lowest income quintile of Americans by $940 on average, or 13% of their after-tax-and-transfer income.

CBO projects that 7.6 million people will lose Medicaid as a result of the Bill. And due to additional cuts and failure to extend premium subsidies, more than 7 million more people would lose coverage from the individual marketplaces, where millions get health insurance, including 3.3 million self-employed people and small business owners.

Providing health insurance isn't just redistribution—it's a critical investment in human capital and safeguards household balance sheets. Studies show that Medicaid coverage is associated with better chronic disease management and improved mental health. Medicaid also leads to sharp declines in medical debt, and completely eliminates catastrophic expenses, improving family balance sheets, access to credit, and financial resilience. Indeed, children with Medicaid coverage pay more in taxes, and receive less in earned income tax credit in adulthood due to higher future earnings.

Reducing wasteful spending has ostensibly motivated the Bill's controversial Medicaid work requirements. But the premise that able-bodied Medicaid enrollees choose not to work is a myth, as the data clearly show. Most of the resulting lost coverage would be among people eligible for Medicaid, for whom documenting work hours is burdensome, if not impractical, given the nature of essential but often informal work. Allowing states to require up to 6 months of employment before eligibility defies the very logic of insulating health and household balance sheets from involuntary disemployment.

At the national level, the Bill’s roughly 1% of GDP increase in annual deficits (d) alone swamps the current margin between r and g. Deficit increases accelerate the trajectory of the rising debt ratio, and the resulting increases in borrowing rates and debt weakens the ability of the government to respond to future economic crises.

Historically, large economic shocks markedly raise (r-g), and especially so during past supply shocks. Shocks also require emergency funding to shorten contractionary spells. The Great Recession and the COVID pandemic represent two “once-in-a-lifetime” recessions in 15 years. As we face heightened global supply chain and climate disaster risks, the US needs to strengthen economic and fiscal resilience, not weaken it with the passage of this Bill.

Broader implications for democracy

In his New York Times opinion piece critical of the Bill, Jason Furman notes that the only thing good about the policy is that it’s Trump’s first major economic policy that doesn't trounce democracy norms. I wish it were so.

In an age of historically high levels of economic inequality, the bill's primary impact will be to exacerbate inequality and weaken the ability of vulnerable households and the government to respond to economic shocks. Inequality is strongly predictive of backslides in democratic institutions, as a recent study by Eli Rau and Susan Stokes shows. Across multiple country settings, they find that on the left and the right, backsliding leaders "play on inequality and deepen polarization by encouraging a sense of grievance among the public. Feelings of being left behind and alienation from elite institutions" means people are more willing to disregard attacks on the press, courts, and other institutions.

The shocking regressivity of this bill also threatens democracy and political stability. And if the symptoms of backsliding seem familiar—and a Bill that so undemocratically serves the interest of wealth at the expense of broader interests becomes law—then it's a dire warning that the backslide has already begun.

Corporate liquid assets as a fraction of short-term liabilities is at the highest level since 1945.

Rohn (2010) also reports smaller to no reductions in investments in response to debt-financed public investments.

It's true that the so-called "Reagan revolution" toppled under it own weight. A big rejection of its impact on the economy and those who shared in it was a good outcome. Nonetheless, the national debt took a hit that was addressed for the better part of a decade after the "great communicator" left office. Many of us hope the draconian features in the new "big" bill, and the many elements that are apparently mostly hidden within it, will meet the same rejection and we'll again agree that we don't have a tax problem, we have a revenue problem that could easily reverse the dunderheaded notion that we invest too much on, you know, the American people!