The Child and Dependent Care Tax Credit Falls Short—But It Could Do Better

Increased generosity and better targeting at adult caregivers would make a difference

High care costs for children and older adults put an increasing strain on American families. Child care remains one of—if not the—biggest expenses that families with young children face, while costs for long-term care for older adults often run into the tens or hundreds of thousands of dollars a year. Although many pundits have commented on the meaningful financial relief that the Child Tax Credit and Earned Income Tax Credit deliver for families, another tax provision of the U.S. social safety net has received far less attention: the Child and Dependent Care Tax Credit (CDCTC), a federal tax credit designed to partially offset working families’ care expenses. In my research, I find that CDCTC benefits increase paid child care use, suggesting that the credit assists at least some working parents in paying for care. Nonetheless, the credit isn’t particularly generous, doesn’t keep pace with inflation, and fails to reach low-income families who do not owe taxes after deductions. It also fails to reach most families providing care to older adults. In this post, I describe the CDCTC, its history and institutional context, and possibilities for better program design.

The CDCTC’s Structure Limits Its Reach

The CDCTC allows households to receive tax benefits against eligible care expenses. Each year, families can claim some care costs on their taxes for up to two household members younger than 13, or for qualifying disabled adults. Household income and care spending determine benefit amounts, and claimants must work to qualify for benefits. For married taxpayers filing jointly, this includes both spouses if neither is disabled.1 Almost any out-of-pocket care expenditures are eligible for the credit, including fees paid to child care providers, adult daycare facilities, and attendants assisting dependents with activities of daily living. To claim the credit, taxpayers must list their earnings, dependent-care expenditures, and dependent-care-providers’ tax identification or Social Security numbers on Federal Form 2441.

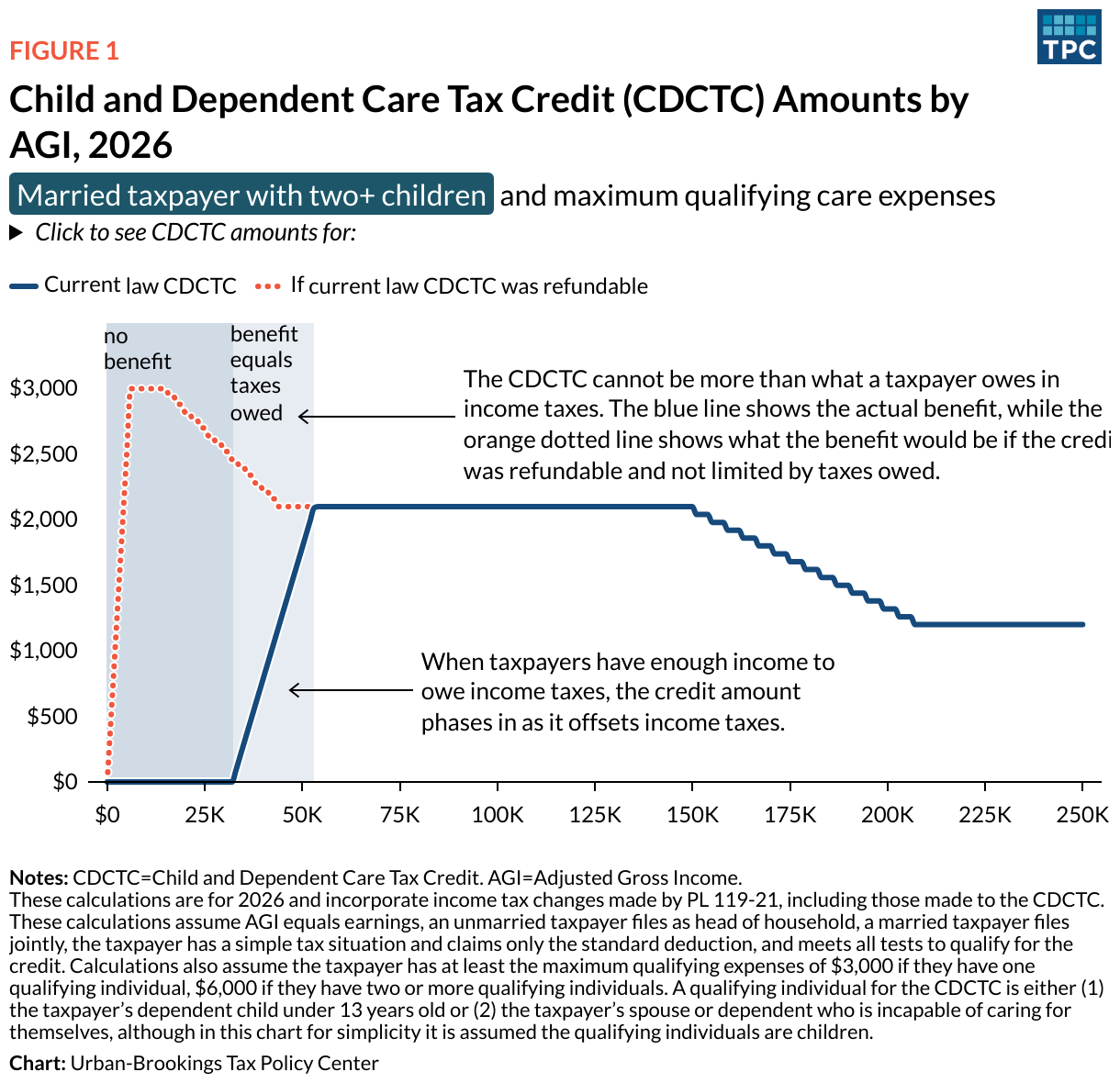

While many families incur eligible expenses, the design of the credit results in it not reaching families that need the most help with care costs. Figure 1 shows that because the CDCTC is nonrefundable, taxpayers’ incomes must exceed the tax filing threshold—$32,000 for married households filing jointly—to be eligible for benefits.2 For taxpayers with incomes above this threshold, maximum benefits increase with income before holding steady at $2,100 ($1,050 per qualifying individual) for households with $54,000 to $150,000 in adjusted gross income. Maximum benefits then decrease but never phase out completely, with the highest-income households still eligible for up to $1,200 in annual benefits.

This structure has two implications. First, although the maximum benefit would be$3,000 if the CDCTC were refundable, in practice, the most a household can get is $2,100. And second, because the CDCTC is nonrefundable, it falls short of helping many lower-income workers, including many of the essential workers who keep our economy going.

Because the CDCTC is nonrefundable, low-income households do not benefit

The CDCTC Isn’t Generous, and Other Programs Don’t Fill Its Gaps

The CDCTC was essentially created by a legal accident. With the goal of helping “families pay employment-related expenses for care of a child,” the CDCTC originated from the United States’ first child care tax break, which dates back to 1954 and the Tax Court case Smith v. Commissioner (1939). In the case, the Tax Court rejected the argument that child care expenditures were a deductible business expense, noting common assumption at the time that such services were “ordinarily rendered without monetary compensation” and that child care was “a personal concern.”3 Though the case was never overruled, Congress eventually recognized the importance and legitimacy of child care expenses and began offering households an itemized deduction of up to $600 in child care expenditures in 1954 ($7,181 in 2025 dollars). In 1976, Congress replaced that deduction with the CDCTC.

As with the federal minimum wage, the CDCTC has never been indexed to inflation, causing its real value to fall over time, and leading to legislative expansion in 1981, 2001, and most recently in 2025, under H.R. 1, the One Big Beautiful Bill Act. Congress also temporarily expanded the CDCTC during 2021 in light of an increased need for caregiving during the Covid-19 pandemic.

With 2021 as an exception, the CDCTC has never covered a large share of care costs, even among households with incomes high enough to benefit from a nonrefundable tax credit. Among such households with children, I find that between 2009 and 2023, benefits covered just 10–20 percent of out-of-pocket child care spending on average, with little change over time. The CDCTC’s lackluster generosity wouldn’t be a big deal if families with caregiving responsibilities could rely on other programs to cover some remaining out-of-pocket expenses. Unfortunately, that generally isn’t the case.

To illustrate the lack of alternative funding for care costs, let’s first look at adult care expenses. Around 50% of Americans turning 65 will eventually require long-term services and supports (LTSS), such as assistance with eating, bathing, and dressing, as well as housekeeping, meal preparation, transportation, and money management services. Medicare and Medicaid coverage for LTSS is limited. Medicare generally only covers LTSS after a hospital stay or medical procedure. Medicaid is the dominant public payer of LTSS, accounting for 61% of direct expenditures. However, because Medicaid eligibility requires income and assets to be below certain thresholds, most Medicaid recipients in need of LTSS first pay directly for services and spend down their wealth until they qualify for benefits. Thus, it is perhaps unsurprising that, in joint work with Yulya Truskinovsky, I find that most care recipients with spouses aged 51–65 do not receive Medicaid. We find that even fewer such households have or use private long-term care insurance. Given the lack of comprehensive public and private insurance coverage for LTSS, researchers estimate the value of private, informal care, such as that provided by family and friends, constitutes ⅓ of total long-term care costs.

Even for small, targeted groups that are eligible for publicly-funded LTSS or child care, access remains limited. For example, Head Start reaches only 1 in 3 income-eligible children, and 13 states had waitlists or froze intake for child care subsidies during 2024. Moreover, around 700,000 individuals have been on waiting lists for Medicaid Home- and Community-Based Services in recent years.

If means-tested or otherwise targeted support for families with care expenses is limited, general support is virtually nonexistent. In fact, the CDCTC and dependent care flexible spending accounts (FSAs) are the only federal programs that directly subsidize out-of-pocket care expenditures. (While taxpayers may receive benefits from both FSAs and the CDCTC, they can’t double count expenses across the two dependent-care subsidy programs.) Like the CDCTC, dependent care FSAs have limited reach: fewer than half of civilian workers have access to these accounts, and families must determine FSA contributions at the beginning of the year. Estimating annual care expenses generally isn’t too difficult for families with ongoing child care expenses—but it’s virtually impossible for families with a loved one who, say, unexpectedly experiences a major medical event that requires caregiving responsibilities to begin midyear. The bottom line is that existing policies to support families with caregiving responsibilities are piecemeal and limited in scope.

How to Build a Better CDCTC

Refundability

The CDCTC could play a bigger role in making caregiving in the U.S. more affordable. Importantly, the CDCTC already exists as a federal policy lever, and it’s often easier politically to amend an existing program than to create an entirely new one. In my research, I use policy simulations to estimate how changes to its structure could better meet the needs of families with care responsibilities. For example, I estimate that, all else equal, if the CDCTC were made refundable—which would allow lower-income households to receive tax refunds—an additional 1 in 20 single parents would gain eligibility. Refundability likely wouldn’t be very expensive— the Joint Committee on Taxation estimates that the much larger increase in CDCTC generosity during 2021 cost the federal government $8 billion. This compares to more than $110 billion for the Child Tax Credit expansion that took place at the same time.

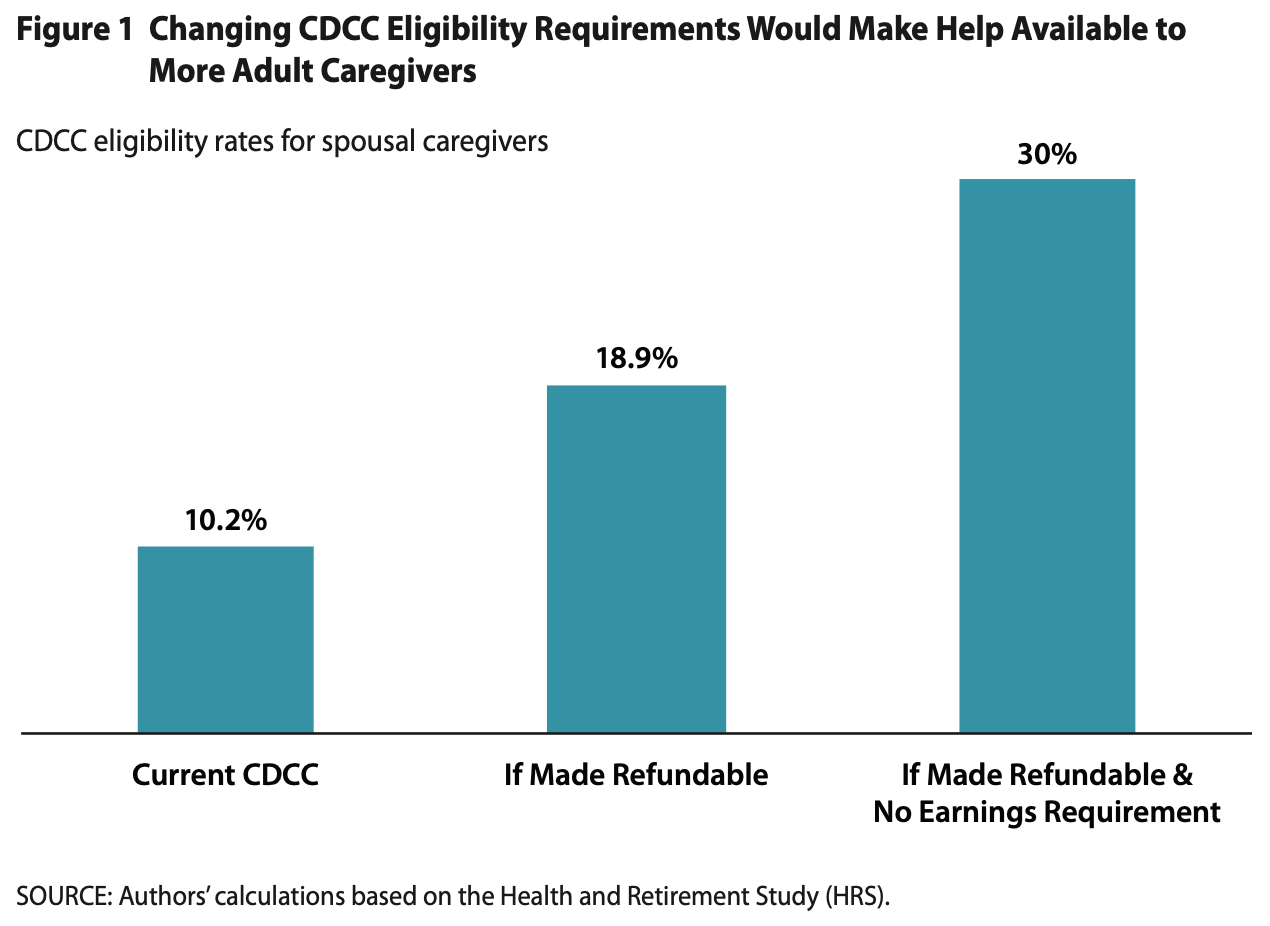

Turning to adult caregivers, Yulya Truskinovsky and I find that refundability would approximately double the number of eligible spousal caregivers. It would especially benefit caregivers who are nonwhite, have lower incomes, and—at least among those caring for adults—have more intensive caregiving responsibilities. Hence, refundability—a straightforward change in the CDCTC’s design—would benefit many caregivers currently experiencing the largest careburden.

Different Eligibility Requirements for Adult Caregivers

Another possible CDCTC design change would be to separate the tax program for child and adult care recipients. The CDCTC was designed primarily to aid parents facing child care costs, but a different tax credit—either the CDCTC or a separate credit for adult caregiving split off the CDCTC—could better meet the needs of those caring for adults. Truskinovsky and I examine tax program changes that could better retrofit the CDCTC for adult caregivers. For adult caregivers, we home in on the CDCTC’s earnings and coresidency requirements. Adult caregivers tend to be further along in their careers than parents of young children, and we document that, in many cases—including for 95% of parental caregivers—they do not live with their care recipients. As shown in Figure 2, simultaneously making the CDCTC refundable and lifting its earnings requirement would triple the number of eligible spousal caregivers aged 51–65, all else equal. While these policy changes would increase tax expenditures, given the relatively modest estimated cost of the COVID-19 temporary CDCTC expansion, as well as state cost-savings associated with keeping older adults out of costly, publicly-funded institutional care, lifting such eligibility requirements for adult caregivers likely would be relatively inexpensive.

Truskinovsky and I also find that in practice, lifting the coresidency requirement wouldn’t increase eligibility all that much: the CDCTC only subsidizes out-of-pocket spending, and institutional care is largely funded by Medicaid. Nonetheless, modifying the CDCTC to make it a more effective tool for adult caregivers could reduce reliance on Medicaid and support the broader long-term care system.

Increases in Generosity

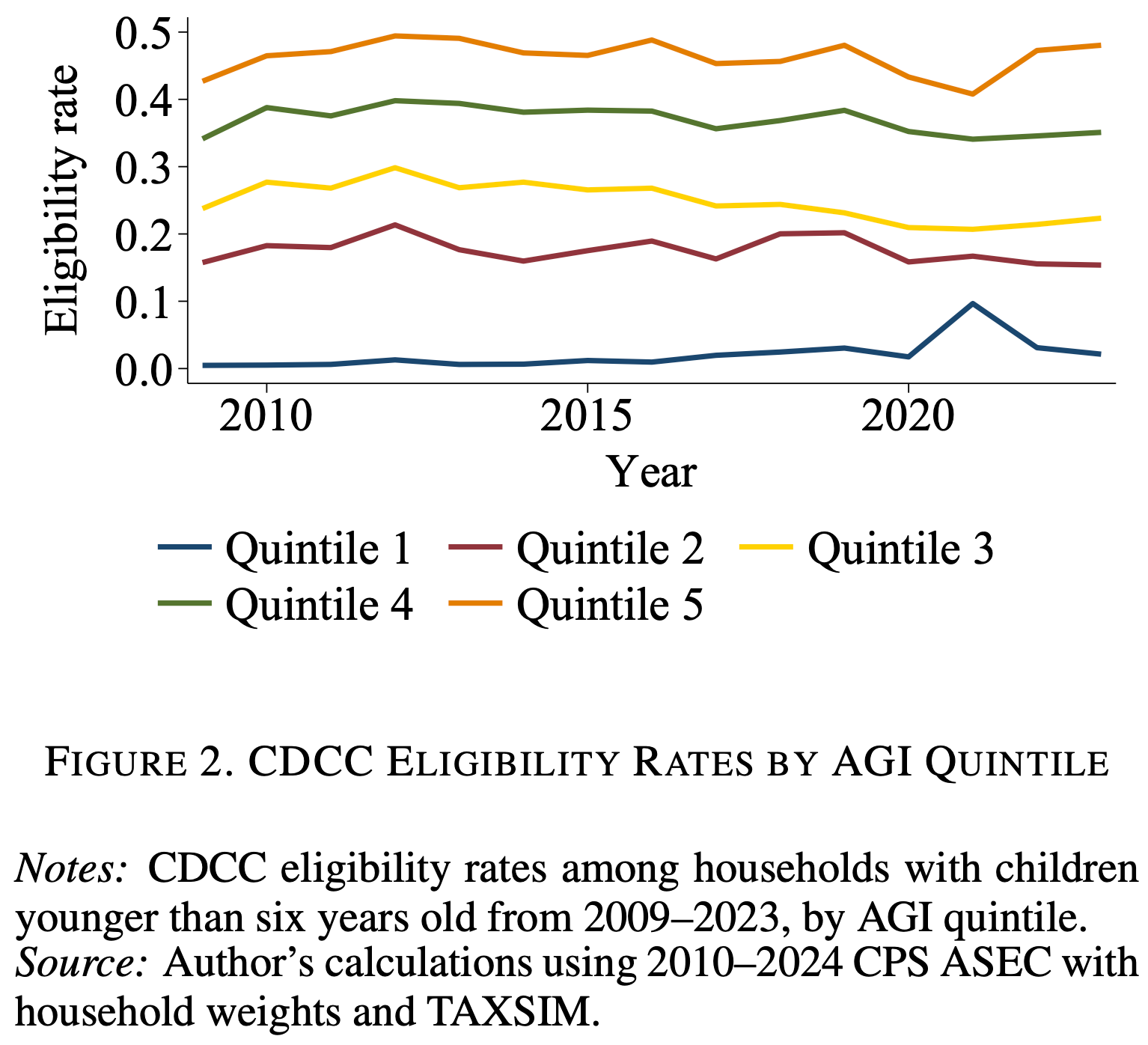

A third potential CDCTC design change is making it more generous. Fortunately, we really don’t have to guess what would happen if the CDCTC were expanded, because this is exactly what happened during the COVID-19 pandemic. In other work, I examine lessons learned from the temporary CDCTC expansion that occurred in 2021. Specifically, because of the increased need for caregiving supports due to Covid-19, the American Rescue Plan Act of 2021 (ARPA) made the CDCTC refundable and increased the maximum benefit to $4,000 per qualifying individual—but only for 2021. My estimates in Figure 3 show that the eligibility rate for the lowest income quintile spiked in 2021, increasing by 8 percentage points to 10%. (The dip in the eligibility rate for the highest income quintile resulted from temporarily capping CDCTC eligibility to households with incomes below $400,000.) In other words, as expected, refundability increased the lowest-income households’ eligibility rate by 400%, while leaving eligibility unaffected for virtually all other households.

Refundability increased low-income households’ CDCTC eligibility during 2021

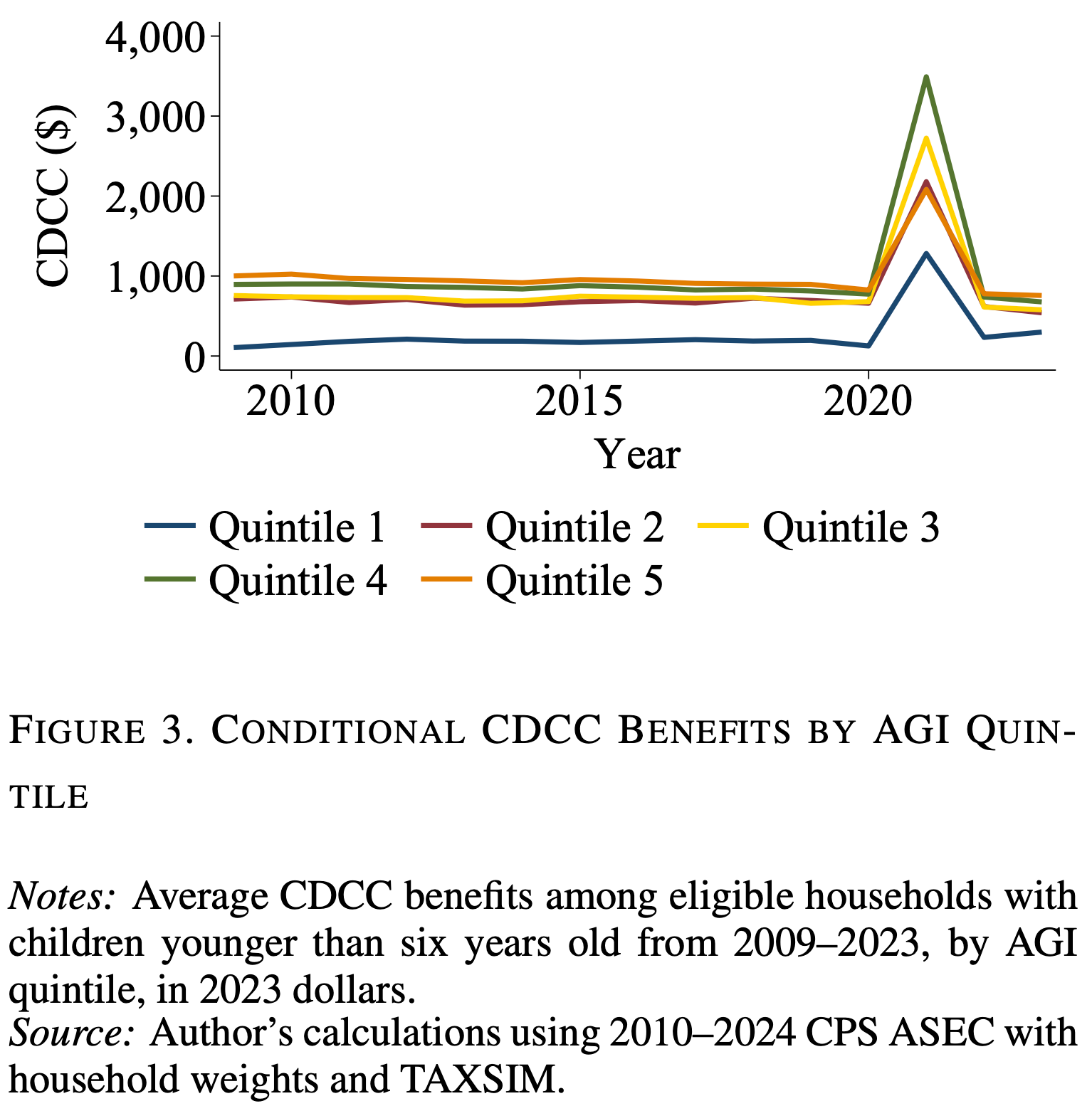

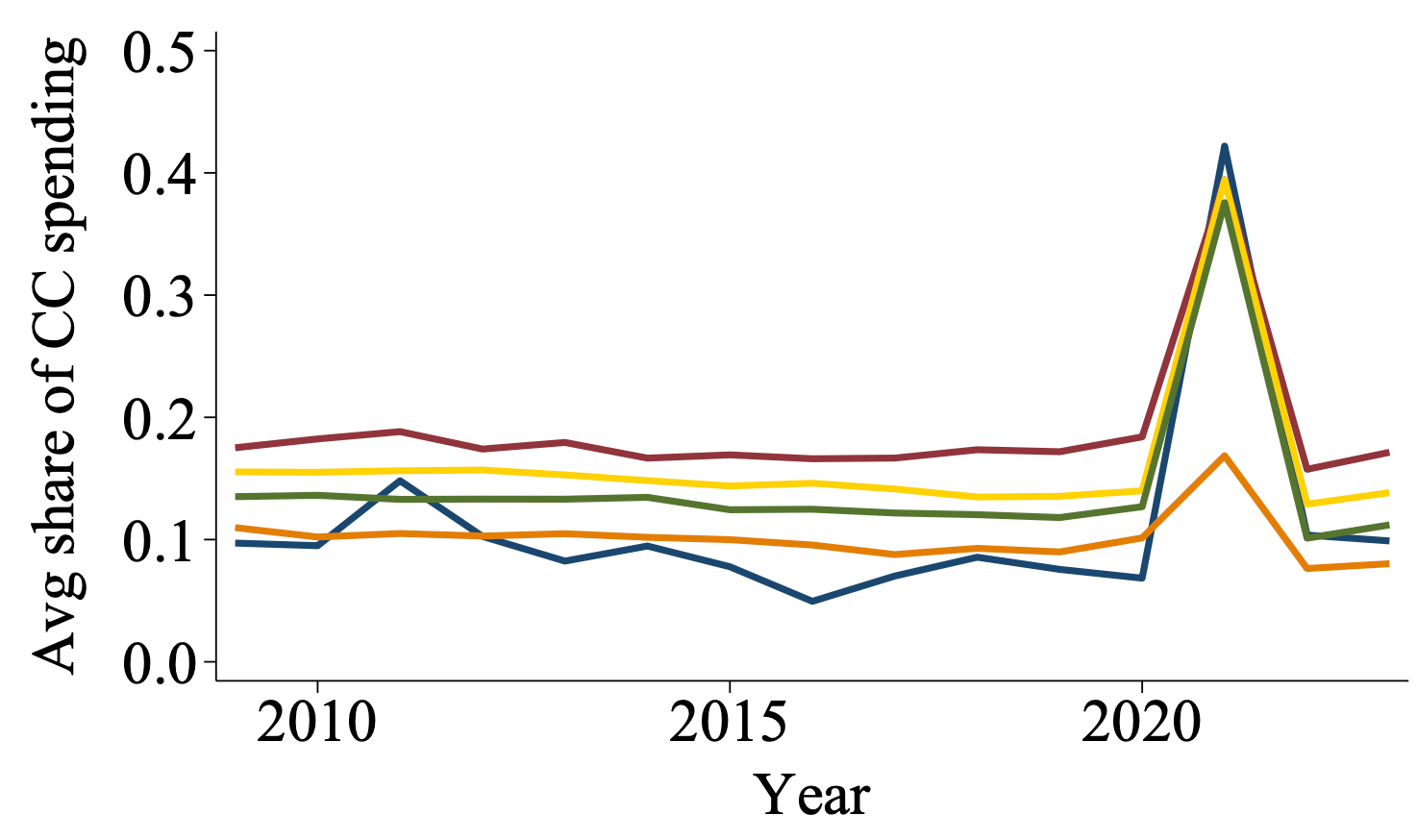

The 2021 CDCTC expansion also provides a blueprint for a credit that’s generous enough to make a difference to family budgets. In Figure 4, I estimate the size of CDCTC benefits among eligible households with young children by income quintile. I find that, during 2021, average benefits range from about $1,300 for the lowest-income households to about $3,500 for households in the second-highest quintile. On average, these amounts cover around 40% of child care spending for all but the highest-income households.

CDCTC benefits covered 40% of child care spending during 2021

Conditional CDCTC benefits as a share of child care spending by income quintile

The CDCTC isn’t a Silver Bullet, But it Could Be More Effective

While the federal CDCTC isn’t a comprehensive solution to America’s caregiving crisis, it has the potential to serve as a politically feasible and well-targeted tool for reducing care costs and promoting work among households with care responsibilities. Unfortunately, it has some major design flaws that impede its generosity and reach.

The good news is that states are leading the way in experimenting with their own care credits.

About half of states offer supplements to the federal CDCTC, and a handful offer tax credits for adult caregivers. The design of these tax credits can go a long way toward making care affordable for families that need it.

To illustrate this point, take two states—Wisconsin and Pennsylvania—that significantly expanded their state supplements to the federal CDCTC in recent years. Wisconsin increased the generosity of its state CDCTC to a maximum of $3,500 per qualifying individual. That’s a very generous headline sum compared to the federal maximum of $1,050 per qualifying individual. However, the credit is nonrefundable and does nothing for the state’s lowest-income families. Meanwhile, Pennsylvania increased the generosity of its state CDCTC to a maximum of $1,050 per qualifying individual. While Pennsylvania’s credit initially looks less generous than Wisconsin’s, it’s fully refundable and brings meaningful financial relief to the state’s lowest-income families, for whom care costs can pose the largest cost burden.

When good care is affordable, the benefits extend beyond just parents and other caregivers. State policymakers who implement CDCTCs that are inclusive and generous help to keep older adults out of even more costly, publicly-fundedinstitutionalcare. And their investments in child care can produce lasting social and economic returns—enabling more parents to work, benefiting employers, boosting the economy, and leading to long-term benefits for the next generation. Thus, federal policymakers who want to make the federal CDCTC work should look to states that are leading the charge in offering care credits that make a difference and foster inclusive economic growth.

If a claimant is a full-time student, the Internal Revenue Service imputes monthly earnings for the purpose of the credit at $250 (for households with one qualifying individual) or $500 (for two or more qualifying individuals).

Households married filing separately typically are ineligible for CDCTC benefits, although benefits generally don’t depend on filing status.

Smith V. Commissioner, 40 B.T.A. 1038 (1939).

| A guest post by

|